Do Global Accountants Have US GAAP Certification? What Finance Leaders Need to Know

The honest answer to whether global accountants understand US GAAP – credentials, training infrastructure, how to verify it, and what the data from real placements shows.

Written by

MAVI

Published On

June 23, 2026

Many global accountants are US GAAP proficient – and some are more practiced in applying specific GAAP standards than their US-based counterparts at comparable experience levels. The distinction is in how they were trained. Big 4 firms operate large practices in international hubs that use the same US GAAP frameworks as their US offices, and certain global credentials and distinctions study and apply GAAP-aligned standards. The knowledge is in the work history, not the location.

That said, "global accountant" is not a monolithic category. It covers everyone from a deeply experienced Big 4 alum with a decade of US company engagements to a junior data-entry resource at a legacy BPO who has never touched a revenue recognition schedule. The gap between those profiles is enormous, and the GAAP question resolves very differently depending on which type of talent you're actually evaluating.

Why the Skepticism Exists – and Where It's Warranted

The concern about GAAP knowledge in global accounting talent isn't baseless. The legacy global accounting model – shared-resource BPO teams running basic transactional functions – was genuinely weak on technical accounting. Those teams were built to handle high-volume data entry at low cost, not to apply judgment-intensive GAAP standards.

Many CFOs who are skeptical of global GAAP knowledge had their first experience through that model. The skepticism is a reasonable inference from it. The problem is applying it uniformly to global accounting talent in 2026, when the professional landscape has changed significantly.

The relevant question isn't whether global accountants as a category know US GAAP. It's whether the specific candidate you're evaluating has the training, credentials, and engagement history that produce genuine GAAP proficiency. That's a sourcing and vetting question, not a geography question.

Where Global GAAP Knowledge Actually Comes From

Big 4 training

Big 4 training runs on the same frameworks, just different locations. Deloitte, PwC, KPMG, and EY all operate large practices and key talent markets that handle US client engagements directly. The training methodology, quality standards, and GAAP frameworks applied in a Big 4 Manila audit engagement are the same as those applied in New York. An accountant who spent four years at PwC Manila on US tech company audits has applied ASC 606, prepared audit workpapers, reviewed revenue recognition schedules, and had their GAAP judgments challenged by senior reviewers and US partners.

The Philippine CPA

The Philippine board exam tests technical accounting knowledge against PFRS – standards closely aligned with IFRS and, for US-client work, US GAAP. The pass rate is consistently below 30%, making it a genuinely rigorous credential. Filipino CPAs working on US company engagements apply US GAAP directly and learn the differences between frameworks as a practical matter.

The Indian CA

The ICAI Chartered Accountant credential is technically demanding in ways that surprise people unfamiliar with it; completion rates historically run in the 5–15% range across all levels. Indian CAs who work at Big 4 India offices on US client engagements apply US GAAP directly. Many have also pursued the US CPA credential, particularly those targeting careers with US multinational companies.

Direct US company engagement history

Beyond credentials, the clearest indicator of practical GAAP proficiency is what a candidate has actually done. An accountant who has spent three years running month-end close for a US SaaS company – managing deferred revenue schedules, preparing board reporting packages, supporting external auditors – has more applied GAAP experience than their credentials alone suggest.

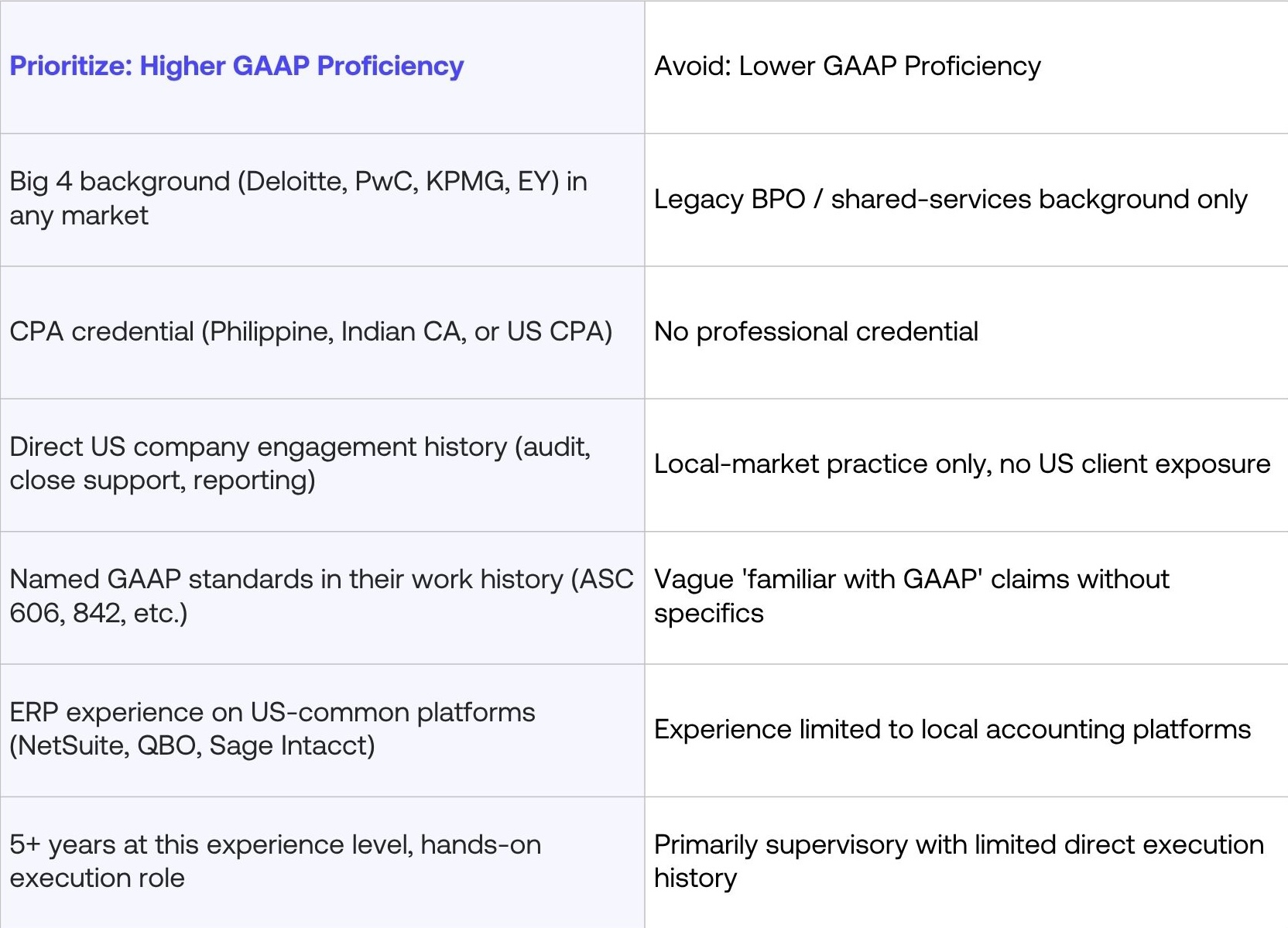

The Profiles That Have It vs. the Ones That Don't

The global talent pool is not uniform. Here's how to think about which profiles are likely to have genuine US GAAP proficiency and which ones are likely to struggle:

The profiles on the left are common in the experienced global talent pool. They are not the majority of all offshore accounting candidates, which is exactly why vetting rigor matters so much. The difference between a marketplace that admits 2% of applicants after multi-round technical assessment and one that accepts 40% after a resume screen shows up directly in which column the placed candidates fall into.

How to Verify GAAP Proficiency

Generic familiarity questions tell you nothing – every candidate will say yes. Scenario-based questions reveal whether the knowledge is real.

For revenue recognition (ASC 606):

"Walk me through how you'd handle a 12-month software subscription paid upfront. What entries do you make at signing, and how does the balance sheet change month to month?" A candidate with real ASC 606 experience will walk through the deferred revenue liability, the monthly release, and contract-end treatment without prompting. Someone coached on terminology gives you a framework description that falls apart under a follow-up.

For month-end close:

"Tell me about a close where something didn't balance – what was it, how did you find it, and what changed afterward?" This is hard to fake because it requires a specific memory. How they describe the root cause, what they actually checked, and what they documented tells you a lot.

For audit readiness:

"If our external auditors asked for support on our accrued liabilities balance, what would you pull together?" An accountant who has actually prepared PBC schedules knows what goes in the package. Someone who hasn't prepared this stays in generalities.

On any answer that sounds right, follow up:

"Can you walk me through a specific example from a previous role?" The shift from theoretical to specific is where surface familiarity breaks down.

Why Provider Quality Is Everything

A global accountant placed through a pre-vetted marketplace that tests for GAAP application is a fundamentally different hire from one placed through a legacy staffing agency that screens on resume and availability.

MAVI's admission process tests for US GAAP knowledge through scenario-based technical assessment. Fewer than 2% of applicants are admitted. When evaluating any global talent provider, ask specifically how they test for GAAP knowledge. "We verify credentials" is not the same as "we assess whether candidates can apply ASC 606 correctly in a scenario." The former tells you someone passed an exam. The latter tells you whether they can handle your close. Book a call to learn more about our vetting process or to take a look at profiles of global accountants who can work with US GAAP standards.

Many do. Global accountants with Big 4 training, CPA or CA credentials, and direct US company engagement history are US GAAP proficient in a practical sense – having applied ASC 606, ASC 842, accrual accounting, and audit procedures in live environments. What varies is sourcing quality, not geography.

Can I trust a global accountant to handle US GAAP financial reporting?

Yes, when the candidate has the right background and has been properly vetted. Finance leaders companies MAVI has worked with, such as Public.com and Athena Club, all had concerns going in – and all reported those concerns resolved quickly once they worked with the placed accountant.

How do Big 4 firms train global accountants in US GAAP?

Big 4 firms operate international practices that handle US client engagements directly, using the same training methodology and GAAP frameworks as their US offices. An accountant who spent four years at PwC in India on US tech company audit engagements has applied ASC 606, prepared GAAP-compliant workpapers, and had their judgments reviewed by US partners.

What credentials should I look for in a global accountant for US GAAP work?

Credential plus engagement history. A CPA-equivalent or adjacent credential alongside a Big 4 background with US client history, direct experience with the GAAP standards relevant to your business, and ERP proficiency in your specific systems. Verify with scenario-based questions, not just credential confirmation.

How does MAVI verify GAAP proficiency in global candidates?

Through scenario-based technical assessment of how candidates apply GAAP standards – not just whether they can describe them – alongside background screening, behavioral interviews, communication assessment, ERP verification, credential checks, and background checks. Fewer than 2% of applicants are admitted. When MAVI presents candidates, the GAAP verification is already done.